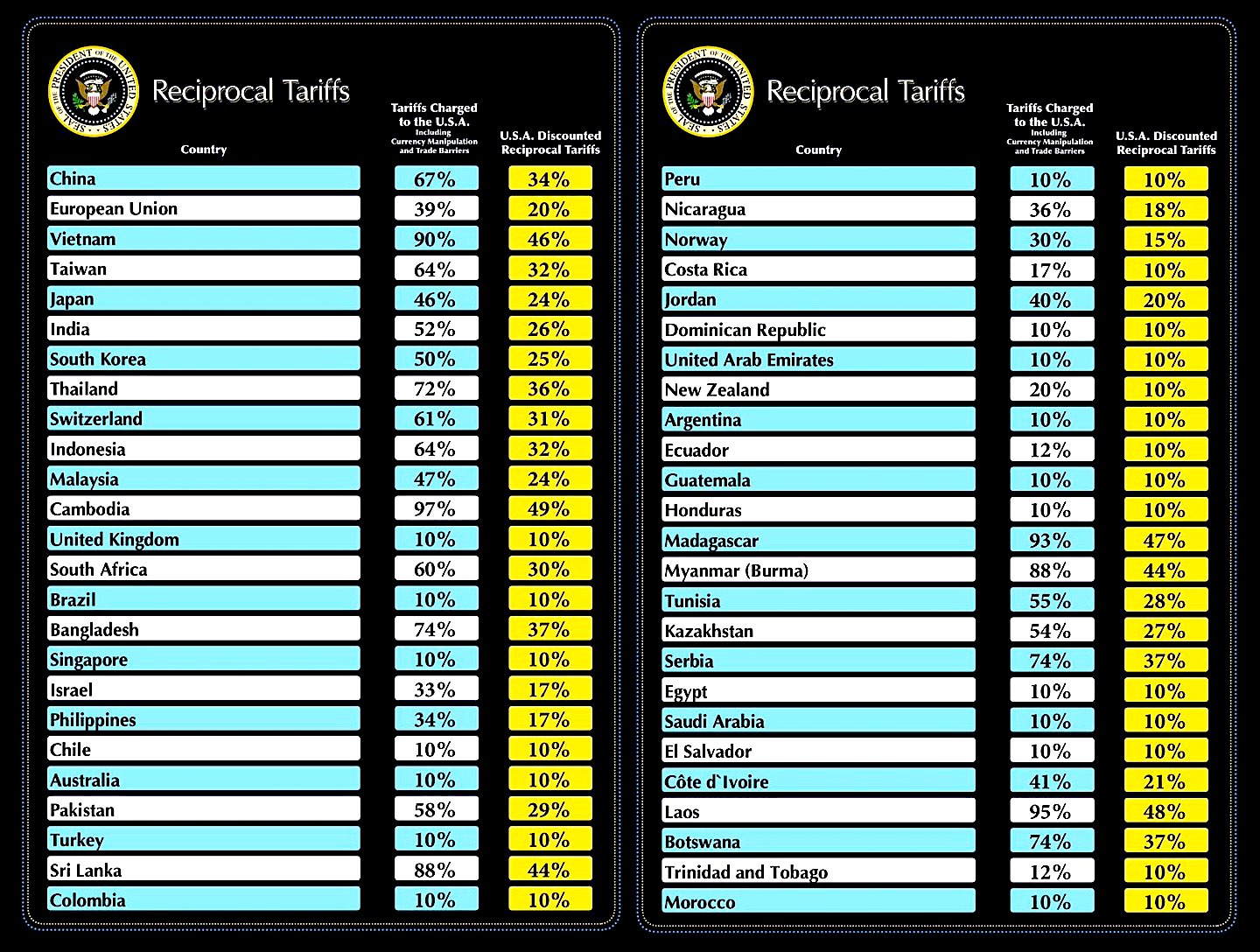

I am not an expert in economics, and I am not interested in a political discussion here, so I simply asked AI, "How will the new Trump tariffs impact the camera and lens imports to the US?". Here is the AI answer:

The new Trump tariffs, as of April 2, 2025, will likely have a notable impact on camera and lens imports to the U.S., particularly from key manufacturing hubs like Japan and China. Here’s a breakdown of the effects:

Higher Import Costs: The tariffs include a 24% increase on camera products from Japan and a 34% rate on goods from China, plus a 10% baseline tariff on imports from all trading partners. This directly raises the cost of bringing in cameras, lenses, and components from major players like Canon, Nikon, Sony (Japan), and third-party lens makers in China. For example, a lens or camera body that cost $500 to import could now face an additional $120-$170 in tariffs, depending on its origin.

Rising Consumer Prices: Historical data from Trump’s earlier tariffs (e.g., 2018-2019) shows that U.S. consumers typically absorb most of these costs. Importers and retailers are likely to pass on the tariff burden, potentially increasing the price of a $1,000 camera to $1,200-$1,340, factoring in the tariff, shipping, and taxes. This aligns with projections from groups like the Consumer Technology Association, which warned of significant price hikes in tech-related imports.

Supply Chain Shifts: Manufacturers may try to offset costs by relocating production. Many Japanese firms already moved some factories to Southeast Asia (e.g., Thailand) during Trump’s first term to dodge China-specific tariffs. However, if critical components still come from China, the 34% tariff applies, limiting the relief. Building U.S.-based production isn’t a quick fix—optics manufacturing requires specialized skills and infrastructure the U.S. currently lacks.

Inventory and Market Reactions: Uncertainty around tariff exemptions (e.g., temporary relief for Canada/Mexico auto imports) could prompt importers to stockpile goods pre-tariff, a trend seen in late 2024 with consumer hoarding. This might delay price spikes, but once stockpiles run dry, costs will climb. Demand could also soften if U.S. prices outpace those in untariffed markets like Europe.

No Quick Domestic Boost: Trump’s tariffs aim to spur U.S. manufacturing, but the camera industry has little domestic presence. Unlike steel or cars, camera production can’t easily shift stateside due to missing expertise and supply chains, meaning imports remain the lifeline—and the target of cost increases.

In short, expect pricier cameras and lenses in 2025, with limited immediate relief from domestic production. Manufacturers might eat some costs to stay competitive, but the bulk will likely hit U.S. buyers, echoing patterns from past tariff rounds where consumer prices rose without significant job gains in affected sectors. Retaliatory moves from Japan or China could further complicate the picture, but for now, it’s a cost-driven story.

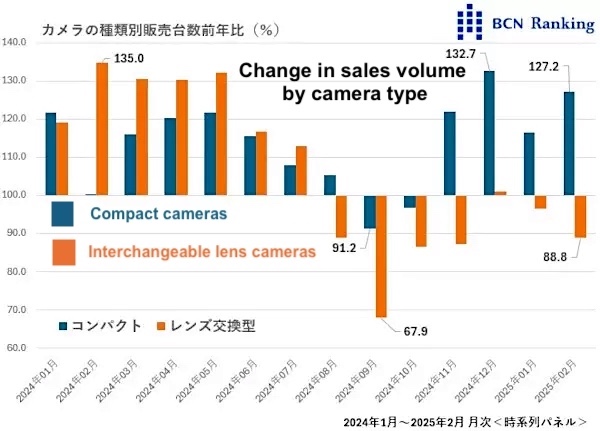

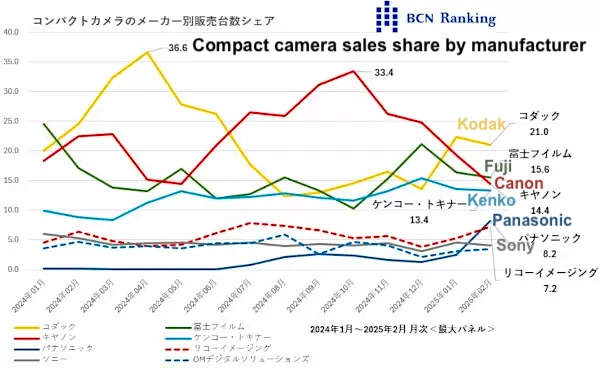

BCN Ranking is making the case that compact fixed-lens cameras are becoming more popular, while interchangeable-lens cameras are starting to lose their popularity:

"Interchangeable lens cameras are starting to run out of steam. Sales have been declining year-on-year since last summer. Interchangeable lens cameras account for more than 60% of the market in terms of sales value.

Meanwhile, compact cameras are growing. Since last November, sales have been increasing by double digits year-on-year. As of February, compact cameras accounted for 71.0% of sales in terms of unit sales and 37.8% in terms of sales value. They are still the mainstream camera in terms of unit sales. There is a strong demand for cameras that are cheap, small, light, and can take photos with decent image quality, rather than expensive, large, and heavy interchangeable lens cameras. However, manufacturers have decided that compact cameras cannot compete with smartphones, whose camera functions have evolved significantly. They have thrown in the white flag and drastically narrowed down their compact product lineup."

BCN+R Camera Market Report (March 23, 2025)

Decline in Interchangeable Lens Cameras:

Sales have been decreasing since summer 2024.

High prices and inflation have dampened consumer demand.

Post-pandemic surge in camera purchases has faded.

Resurgence of Compact Cameras:

Sales have been increasing since November 2024, with double-digit growth continuing into February 2025.

Compact cameras accounted for 71.0% of unit sales and 37.8% of market value in February.

Consumers prefer affordable, lightweight options with good image quality.

Market Trends & Key Players:

Kodak – Led in unit sales (over 20% share), driven by the PIXPRO FZ55 (~20,000 yen).

Canon – Held the top market share from July to December 2024, fueled by the 2016 IXY 650.

Fujifilm – Climbed to second place in February, thanks to the instax mini Evo (instant film).

Kenko Tokina – Gained traction with budget models like the KC-03TY (<10,000 yen).

Panasonic – Improved market ranking with the new LUMIX TZ99 (launched in February).

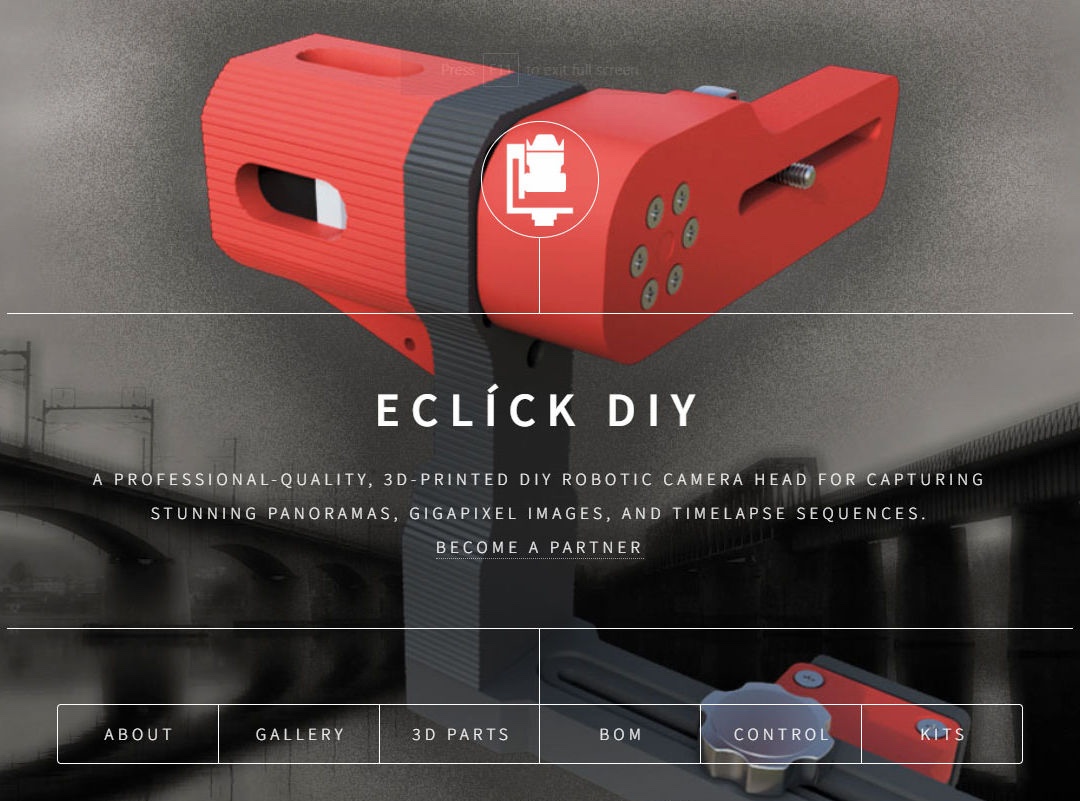

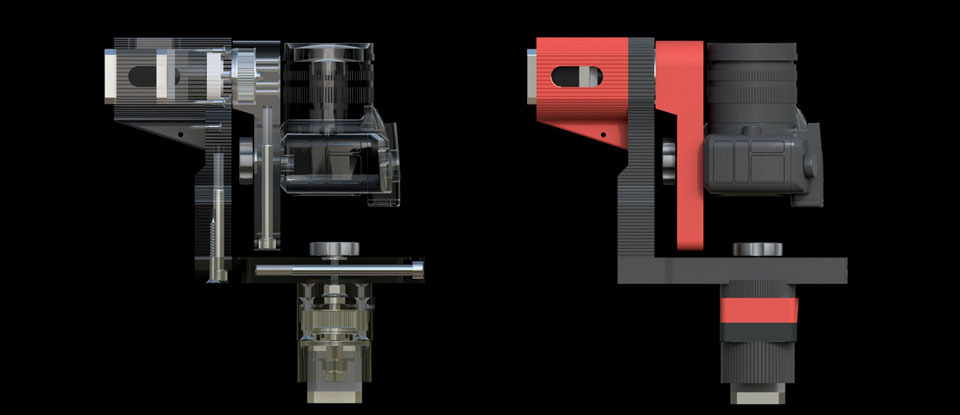

Eclíck released a new 3D-printed, open-source, DIY robotic panorama camera head designed for shooting panoramas, gigapixel images, and time lapse sequences:

Eclíck DIY, 3D printed robotic panorama head

The Eclíck robotic panorama head is a new open-source tool offering photographers and filmmakers an affordable, 3D printed, DIY alternative to expensive commercial options. The Eclíck distinguishes itself through an innovative steel-reinforced design that overcomes the

durability limitations typically associated with 3D-printed equipment. By embedding steel rods within the printed components, the device delivers exceptional strength and precision even when supporting heavy camera gear or operating in challenging conditions.

The system employs a dual-axis movement mechanism enabling photographers to capture flawless 360° panoramas, timelapses, and gigapixel images with precision and ease.

It works seamlessly with all modern DSLR and mirrorless cameras that support a wired remote, ensuring universal compatibility across photography systems. Users can control the Eclíck wirelessly via a built-in web app from any device equipped with WiFi and a web browser, including iPhone, Android, Windows, Linux, and more. This platform-agnostic approach eliminates the need for proprietary apps or specific hardware requirements.

Beyond its performance benefits, the Eclíck prioritizes accessibility in every aspect of the design. All files required to print components are freely available online, and the system utilizes readily available, off-the-shelf parts that are comprehensively detailed in an accompanying bill of materials. This approach eliminates the common frustration of hunting for obscure components that often plagues DIY projects.

The Eclíck has been engineered for straightforward assembly, requiring only basic tools and minimal technical expertise. This consideration extends the potential user base beyond experienced makers to include photography enthusiasts who may be attempting their first DIY equipment build.

And thanks to its fully open-source design, every part can be easily printed and replaced if needed - making the Eclíck the ultimate repairable robotic head.

Technical Specifications:

Dual-axis (pan/tilt) motorized motion system

Steel-reinforced 3D-printed components

Compatible with standard stepper motors

Universal compatibility with modern cameras supporting wired shutter remote

Browser-based wireless control via local WiFi

Cross-platform support (iOS, Android, Windows, Linux, macOS)

Suitable for DSLR and mirrorless camera systems

Load Capacity: 3Kg (6.6lbs)

Open-source hardware and software

Fully repairable with user-printable replacement parts

Complete documentation, printing files, and bill of materials for the Eclíck robotic head are available

at www.Eclick.org.

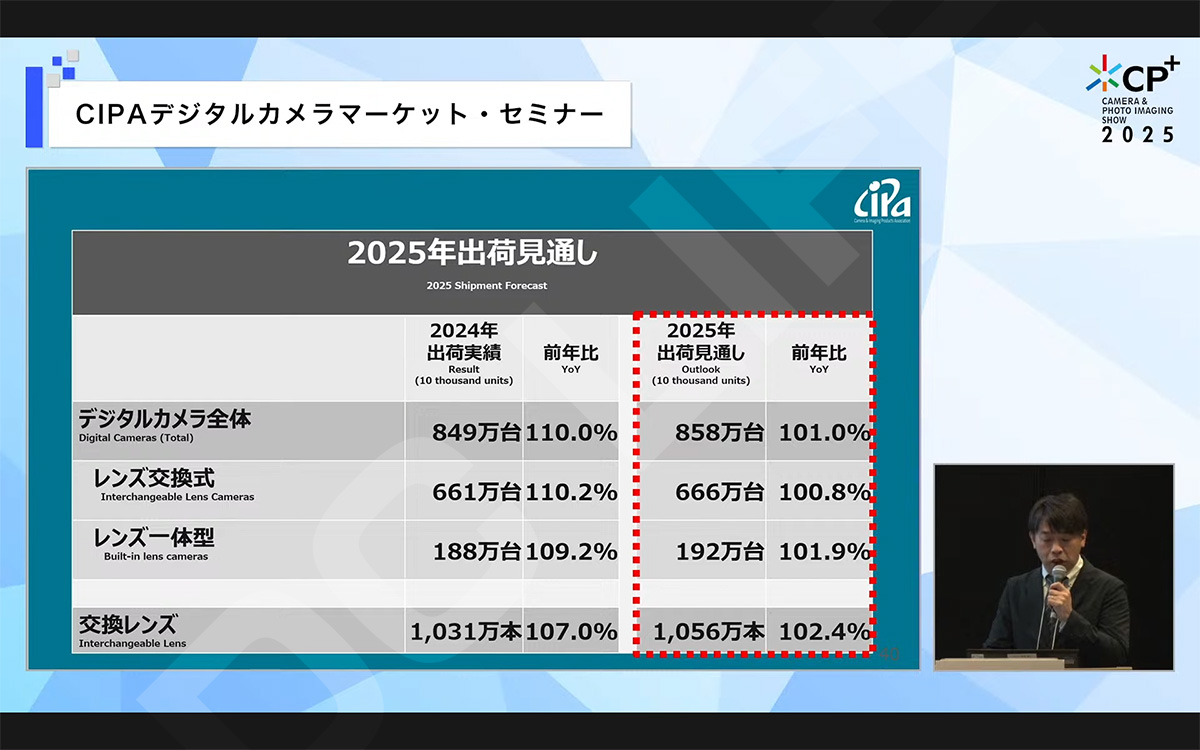

CIPA also revealed their 2025 camera and lens shipment forecast and price graphs:

Shipment forecast for 2025

The graph, presented by CIPA (Camera & Imaging Products Association) at the CP+ Camera & Photo Imaging Show 2025, provides the 2025 shipment forecast for digital cameras, comparing the 2024 results (in ten thousand units) with the 2025 outlook, including year-over-year (YoY) percentage changes. The data is categorized into total digital cameras, interchangeable-lens cameras, built-in lens cameras, and interchangeable lens cameras specifically.

2024 Results (in ten thousand units):

Total Digital Cameras (Total): 84.9 units, with a YoY increase of 110.0%.

Interchangeable-lens Cameras: 66.1 units, with a YoY increase of 110.2%.

Built-in lens Cameras: 18.8 units, with a YoY increase of 109.2%.

Interchangeable Lens Cameras: 1,031 units, with a YoY increase of 107.0%.

2025 Outlook (in ten thousand units):

Total Digital Cameras (Total): 85.8 units, with a YoY increase of 101.0%.

Interchangeable-lens Cameras: 66.6 units, with a YoY increase of 100.8%.

Built-in lens Cameras: 19.2 units, with a YoY increase of 101.9%.

Interchangeable Lens Cameras: 1,056 units, with a YoY increase of 102.4%.

The forecast indicates a modest growth in shipments for 2025 compared to 2024, with all categories showing a slight slowdown in the rate of increase. Total digital camera shipments are expected to rise from 84.9 to 85.8 units (101.0% YoY), interchangeable-lens cameras from 66.1 to 66.6 units (100.8% YoY), built-in lens cameras from 18.8 to 19.2 units (101.9% YoY), and interchangeable lens cameras specifically from 1,031 to 1,056 units (102.4% YoY).

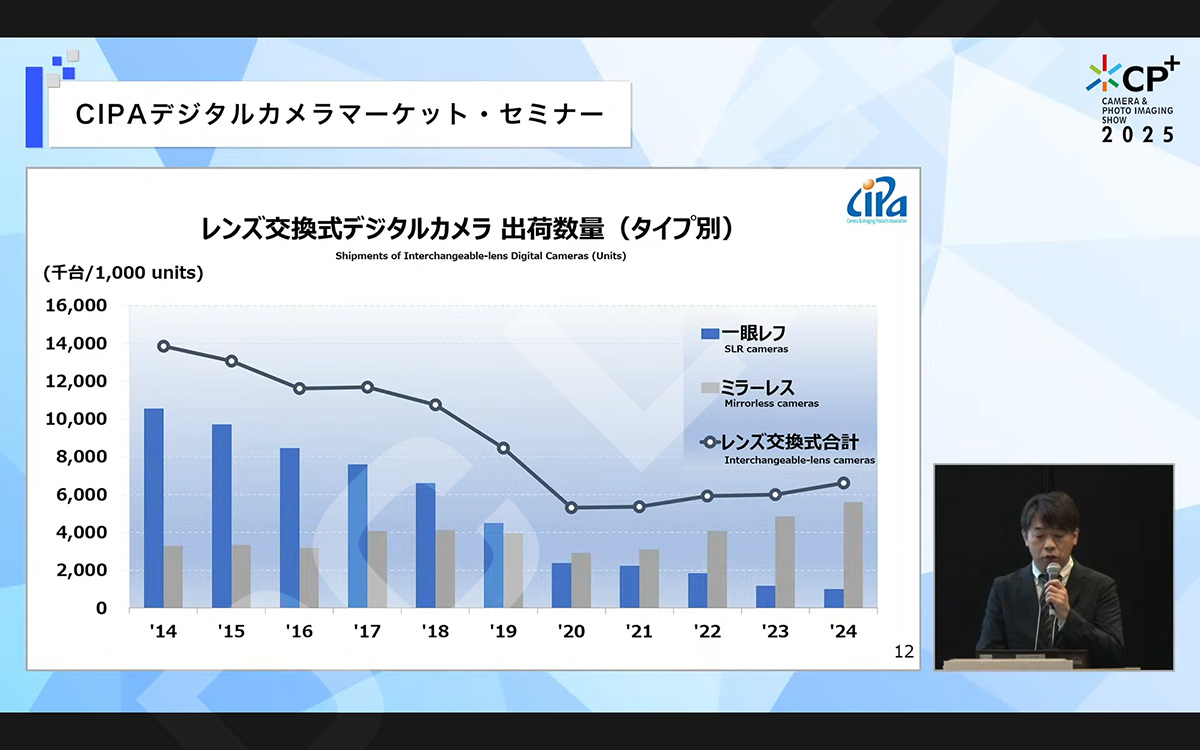

Shipment volume of Interchangeable lens cameras

The graph, presented by CIPA (Camera & Imaging Products Association) at the CP+ Camera & Photo Imaging Show 2025, illustrates the shipments of interchangeable-lens digital cameras (in thousands of units) from 2014 to 2024. The data is categorized into two types: SLR cameras (blue bars) and mirrorless cameras (gray bars), with a line graph representing the total shipments of interchangeable-lens cameras.

2014: Total shipments started at around 12,000 units, with SLR cameras dominating at approximately 10,000 units and mirrorless cameras contributing around 2,000 units.

2015-2017: Total shipments remained relatively stable, fluctuating between 10,000 and 12,000 units. SLR camera shipments stayed high, around 8,000-10,000 units, while mirrorless camera shipments began to grow, reaching about 4,000 units by 2017.

2018-2020: A noticeable decline in total shipments occurred, dropping to around 6,000 units by 2020. SLR camera shipments decreased significantly to around 2,000-4,000 units, while mirrorless camera shipments started to rise, contributing a larger share.

2021-2024: Total shipments showed a slight recovery, stabilizing around 6,000-8,000 units by 2024. Mirrorless camera shipments increased to approximately 4,000-6,000 units, overtaking SLR cameras, which dropped to minimal levels (around 1,000-2,000 units).

The graph indicates a shift from SLR to mirrorless cameras in the interchangeable-lens camera market, with total shipments peaking in the mid-2010s and then declining, followed by a modest recovery driven by mirrorless technology.

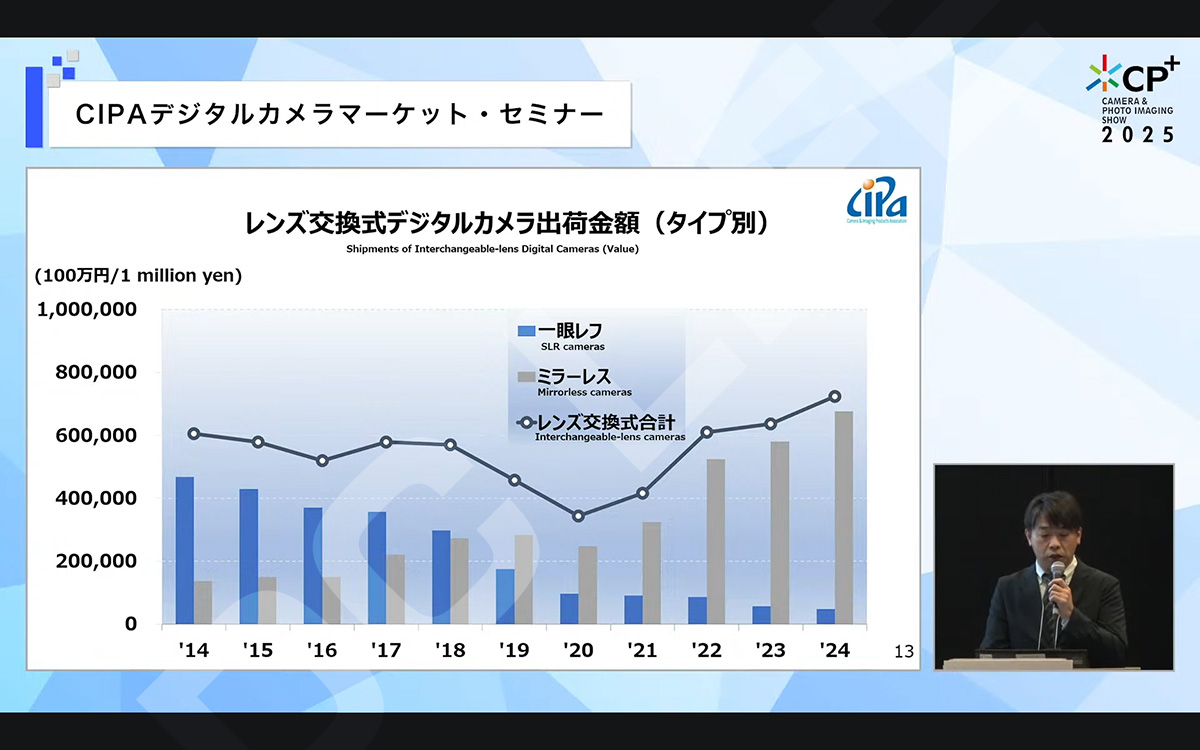

Interchangeable lens digital camera shipment value 2014-2024

The graph, presented by CIPA (Camera & Imaging Products Association) at the CP+ Camera & Photo Imaging Show 2025, illustrates the shipments of interchangeable-lens digital cameras in terms of value (in 100 million yen) from 2014 to 2024. The data is divided into two categories: SLR cameras (blue bars) and mirrorless cameras (gray bars), with a line graph representing the total value of interchangeable-lens cameras.

2014: The value started at approximately 400,000 (100 million yen), with SLR cameras dominating.

2015-2017: The value remained relatively stable, fluctuating around 400,000-500,000, with a gradual decline in SLR camera shipments and a slight increase in mirrorless camera shipments.

2018-2019: There was a noticeable drop in total value, reaching a low of around 200,000-300,000, with mirrorless cameras beginning to gain more market share.

2020-2021: The value continued to decline, hitting its lowest point around 200,000, with mirrorless cameras overtaking SLR cameras in contribution.

2022-2024: A significant recovery is observed, with the total value rising sharply to over 800,000 by 2024, driven largely by a surge in mirrorless camera shipments, while SLR camera shipments remain minimal.

Overall, the graph highlights a shift from SLR to mirrorless cameras and a strong recovery in the market value of interchangeable-lens cameras in recent years.

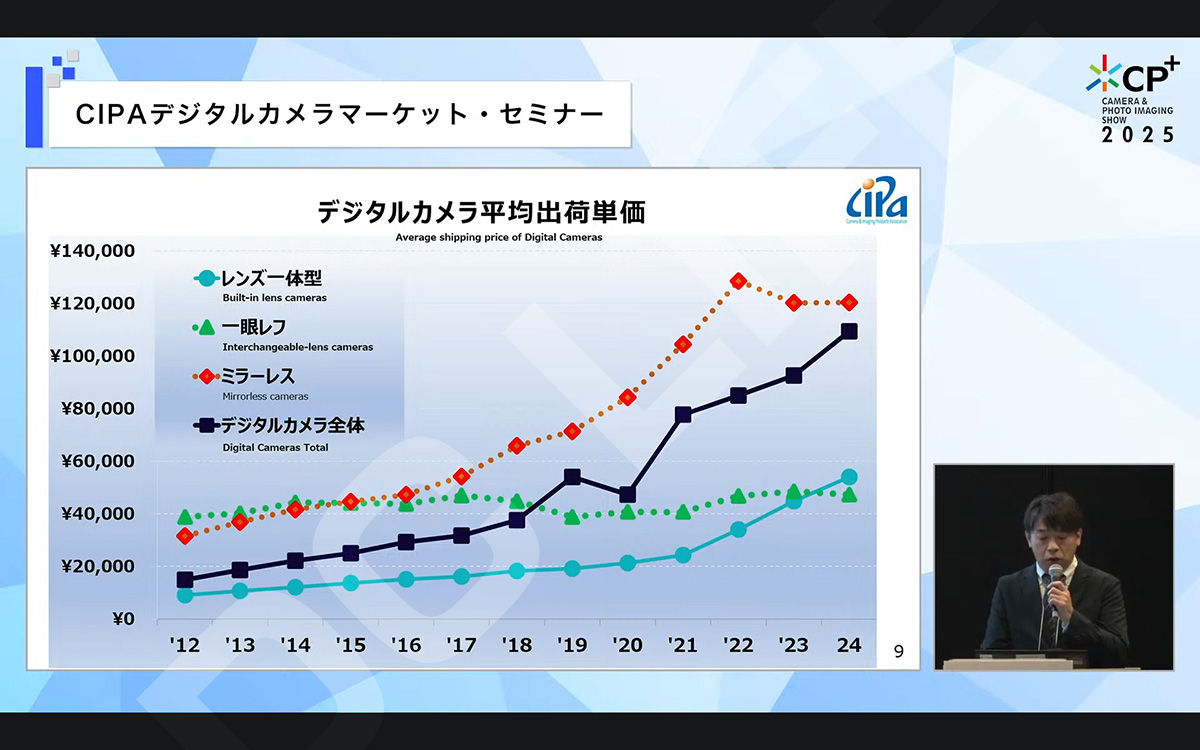

Average shipping cost of digital cameras 2012-2024

The graph, presented by CIPA (Camera & Imaging Products Association) at the CP+ Camera & Photo Imaging Show 2025, displays the average shipping price of digital cameras in yen from 2012 to 2024. The data is categorized into four types: built-in lens cameras, interchangeable-lens cameras, mirrorless cameras, and the overall average price of digital cameras.

2012-2014: The average price for all digital cameras (black line) started around ¥40,000 and remained relatively stable, with built-in lens cameras (cyan line) around ¥20,000-¥30,000, interchangeable-lens cameras (green line) around ¥40,000-¥50,000, and mirrorless cameras (red dashed line) beginning to rise from around ¥60,000.

2015-2019: The overall average price saw a slight decline to around ¥30,000-¥40,000. Built-in lens cameras remained steady at ¥20,000-¥30,000, while interchangeable-lens cameras fluctuated around ¥40,000-¥50,000. Mirrorless cameras showed a steady increase, reaching approximately ¥80,000 by 2019.

2020-2021: The overall average price dipped to its lowest point around ¥30,000. Built-in lens cameras stayed low at ¥20,000-¥30,000, interchangeable-lens cameras dropped to around ¥40,000, and mirrorless cameras peaked at around ¥100,000 before a slight decline.

2022-2024: A significant upward trend emerged, with the overall average price rising to over ¥60,000 by 2024. Built-in lens cameras increased to around ¥40,000, interchangeable-lens cameras rose to approximately ¥60,000, and mirrorless cameras surged to over ¥120,000, driving the overall increase.

The graph indicates a general increase in the average shipping price of digital cameras, particularly driven by the rising cost of mirrorless cameras in recent years.

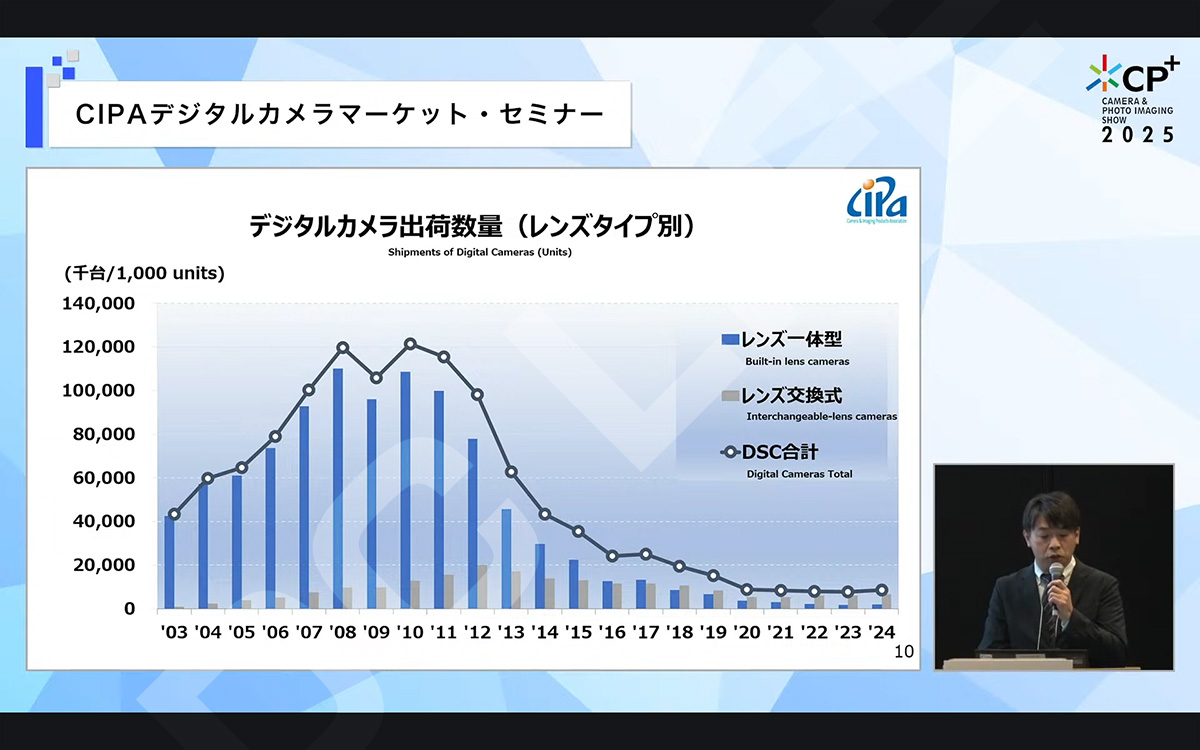

Digital camera shipment volumes from 2003 to 2002

The graph, presented by CIPA (Camera & Imaging Products Association) at the CP+ Camera & Photo Imaging Show 2025, shows the shipments of digital cameras (in thousands of units) from 2003 to 2024. The data is categorized into three groups: built-in lens cameras, interchangeable-lens cameras, and the total digital camera shipments.

2003-2007: Total digital camera shipments (black dotted line) began at around 40,000 units and rose sharply to a peak of approximately 120,000 units by 2007. Built-in lens cameras (blue bars) dominated, contributing the majority of the shipments, while interchangeable-lens cameras (gray bars) started at a low level and remained minimal.

2008-2010: The total shipments reached their highest point, exceeding 140,000 units, driven primarily by built-in lens cameras. Interchangeable-lens camera shipments began to increase slightly but remained a small fraction.

2011-2019: A significant decline occurred, with total shipments dropping to around 20,000-30,000 units by 2019. Built-in lens camera shipments fell sharply, while interchangeable-lens camera shipments saw a temporary rise around 2012-2014 before declining.

2020-2024: The total shipments continued to decline steadily, stabilizing at around 10,000 units by 2024. Built-in lens camera shipments became negligible, and interchangeable-lens camera shipments also dropped to low levels.

The graph highlights a dramatic peak in digital camera shipments in the mid-2000s, followed by a consistent decline over the subsequent years, with built-in lens cameras initially driving the market and interchangeable-lens cameras failing to sustain growth.

2019: A significant decline to 2.316 million units.

2020: Further drop to 1.296 million units, influenced by the COVID-19 pandemic.

2023: Reaching a low of 912,000 units.

2024: A slight recovery to 1.012 million units.

Breakdown by Camera Type:

2018–2021: Compact cameras with integrated lenses accounted for about 60% of shipments, DSLRs 10%, and mirrorless cameras just over 20%.

2022: Mirrorless camera shipments surged, surpassing compact cameras.

2024: Mirrorless cameras constituted 53.6% of total shipments.

Sales Data from BCN Ranking:

Despite the increase in mirrorless camera shipments, actual sales data indicates that compact cameras with integrated lenses continue to dominate, maintaining over 60% of sales from 2018 to 2024.

Mirrorless cameras, while growing from 18.4% in 2018 to 32.3% in 2024, have not exceeded a 30% sales share.

Kumamon

Kumamon